Quick Takes

- Stocks Higher. U.S. equity indices were higher in June as conflict escalated and then de-escalated in the Middle East and congress tries to enact fiscal changes. The S&P 500 rose 5% and the Nasdaq 100 and the Magnificent 7 both rose over 6% as AI optimism continues to drive technology shares.

- Inflation and Interest Rates. The 10Y treasury yield fell in June to 4.2% as the U.S. Senate reviewed and debated the Big Beautiful Bill legislation passed by the House in May. The Fed kept interest rates unchanged and Core CPI inflation remained at 2.8%.

- Apple’s AI Woes. Apple announced in June that it is considering using externally-developed AI models like ones offered by Open AI and Anthropic to power a new version of Siri on its devices instead of an internal model in a major reversal of the company’s AI strategy.

- Big Beautiful Bill. The Senate reviewed the Big Beautiful Bill legislation that the House passed a version of in May. The bill extends the 2017 tax cuts and adds new tax exemptions while cutting Medicaid and other social spending and increasing spending for defense and border security.

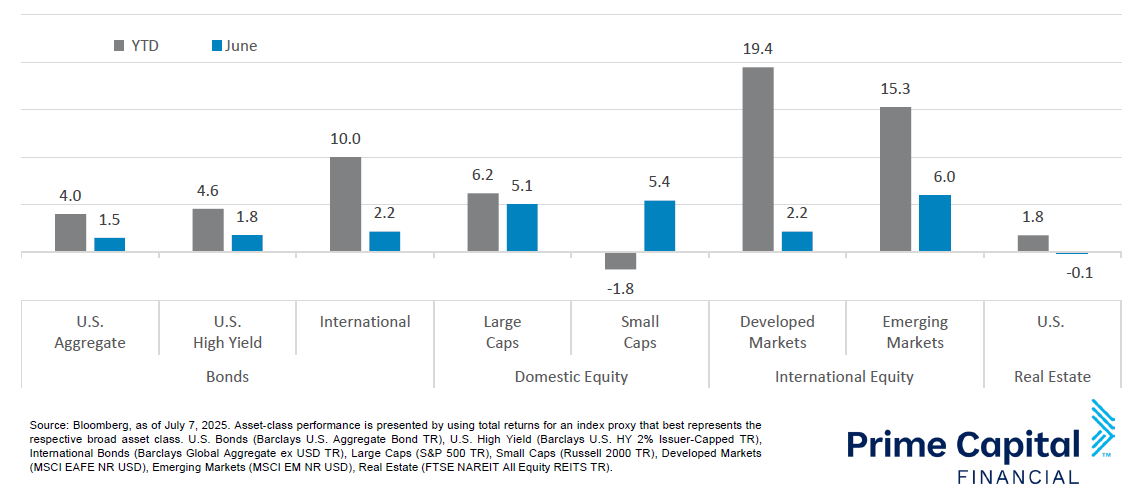

Asset Class Performance

Small caps outperformed large caps in June. U.S. stocks outperformed developed market stocks but underperformed emerging markets as economic data remains mixed and the Fed held interest rates steady. Stocks and real estate were generally higher in May while U.S. bonds fell.

Markets & Macroeconomics

U.S. consumers have become increasingly cautious on spending as retail sales declined in May by 0.9% from April levels marking the second consecutive monthly decline and the largest month-over-month decline in over two years. Motor vehicle and parts stores, food and beverage services, and building and garden materials experienced particularly large declines. Core CPI inflation remained flat, although was below expectations, in May coming in at 2.8% while headline CPI inflation came in at 2.4%. Shelter, medical care services, and education services inflation eased slightly in May while transportation services, transportation commodities, and household furnishings and supplies experienced acceleration in their inflation rates year-over-year, although these changes were slight. Food and energy inflation both accelerated during the month, although energy inflation remained negative. Core PCE inflation came in slightly higher than forecasted at 2.7% and the headline figure came in at 2.3%. In the labor market, the U.S. added 139K jobs in May, mostly in education and health services and leisure and hospitality. Professional and business services experienced a decline of 18K jobs month-over-month as businesses laid off administrative and support staff. The manufacturing also shed 8K jobs and mining and logging each cut 1K positions in May. April’s job additions figure was revised down from 177K new positions to 147K jobs. Initial jobless claims have also been rising in recent weeks, although they declined in the final week of June, with the 4-week moving average now at 245.0K claims. The labor force participation rate fell slightly in May from 62.6% to 62.4% and the unemployment rate remained unchanged at 4.2%. On June 18th, the Fed announced that it was maintaining its policy rate at 4.25-4.50% with the consensus among FOMC participants being that the policy rates will be cut by 50 bps from current levels by the end of 2025. The Fed also reduced its GDP growth outlook for 2025 to 1.4% and increased its PCE inflation projection to 3% with tariffs driving inflation expectations higher.

Bottom Line: The Fed continued to maintain its policy rate in place at the June meeting and reduced estimates for GDP growth while increasing its inflation forecast. Consumers cut back in May while inflation remained unchanged. Initial jobless claims have increased in recent weeks amid slower job growth.