Quick Takes

- Volatile Stocks. US equity indices fell again in March as weak consumer sentiment and tariff worries began to hit the market hard. The S&P 500 fell 5.75% and the Nasdaq 100 fell 7.7%. The Magnificent 7, which has driven the market over the last few years, fell 9.7%.

- Inflation and Interest Rates. The 10Y treasury yield remained flat in March at 4.2% as concerns over the federal budget and finances dominated headlines. Core PCE inflation for February came in above expectations at 2.8% while headline PCE inflation was 2.5%.

- Tariff Unpredictability. President Trump used tariffs on Canada, Mexico, and China in March. He also began to push for reciprocal tariffs on countries that have trade barriers including tariffs or other measures. One threat involved placing a 200% tariff on alcohol imports from Europe, although this never went into effect.

- International Shift. By the end of March, the S&P 500 had fallen 4.6% year-to-date while the STOXX Europe 600 index had risen 5% as investors increasingly began shifting to international assets. A looser fiscal policy in Germany is expected to be stimulative to the European economy.

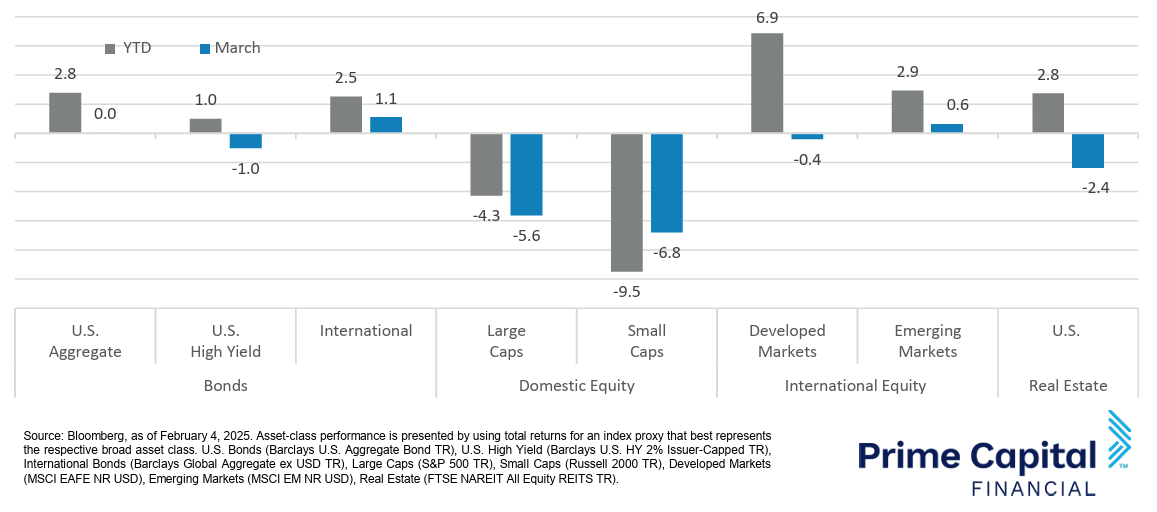

Asset Class Performance

Large caps outperformed small caps in March. US stocks underperformed international stocks, emerging and developed alike, as trade policy uncertainty, headline risks, and weakening consumer sentiment hurt US markets. International stocks were flat in March while international bonds rose and US stocks, bonds, and real estate fell.

Markets & Macroeconomics

New economic data for January indicated higher price inflation and slower job growth than in December, which was a large contributor to investor angst in the stock market during the month. Headline CPI and Core CPI inflation came in ahead of expectations at 3.0% and 3.3% respectively. Headline PPI and Core PPI inflation came in even further ahead of expectations at 3.5% and 3.6% respectively. These data seem to indicate continued challenges with further reduction of inflation back to the Federal Reserve’s 2% long-term target. PCE inflation came in more in line with expectations for the month with Core PCE inflation coming in at 2.6% and the headline figure coming in at 2.5%. On the consumer spending side of things, retail sales fell sharply in January by 0.9% from December’s level, far more than expected. Retail sales excluding car sales also fell by 0.4% versus expected growth of 0.3%. Personal incomes rose 0.9% during the month of January, ahead of expectations, but personal spending fell more than expected dropping 0.2% during the month. Consumer sentiment indicators for February were below expectations as well. In the housing market, new and existing home sales both fell more than expected in January as stubbornly high mortgage rates and real estate prices hurt demand. In addition to inflationary pressures remaining elevated and consumer spending slowing in some areas, job growth slowed in January to 143K versus December’s revised addition of 307K jobs. Despite the lower rate of job growth, unemployment fell and labor force participation rose on the month as unemployment fell in January to 4.0% from 4.1% and the labor force participation rate rose slightly from 62.5% to 62.6%. Wages rose significantly ahead of expectations in January with average hourly earnings increasing 4.1% from a year earlier compared to the forecasted 3.8%. Some trouble could be ahead for labor demand, however, as initial jobless claims came in above forecasted in the last two weeks of the month. The FOMC announces its next rate decision on March 19. Investors are currently expecting a 91% probability of no rate cut in March implying that the Federal Funds target rate will remain at 4.25%-4.50%.

Bottom Line: Unemployment remains low and job creation remains at 100K-150K jobs per month despite a recent slowdown in the overall labor market. Tariffs and trade policy uncertainty have contributed to lower consumer sentiment and household spending growth seems to be slowing.